.svg)

TL;DR: Key Points

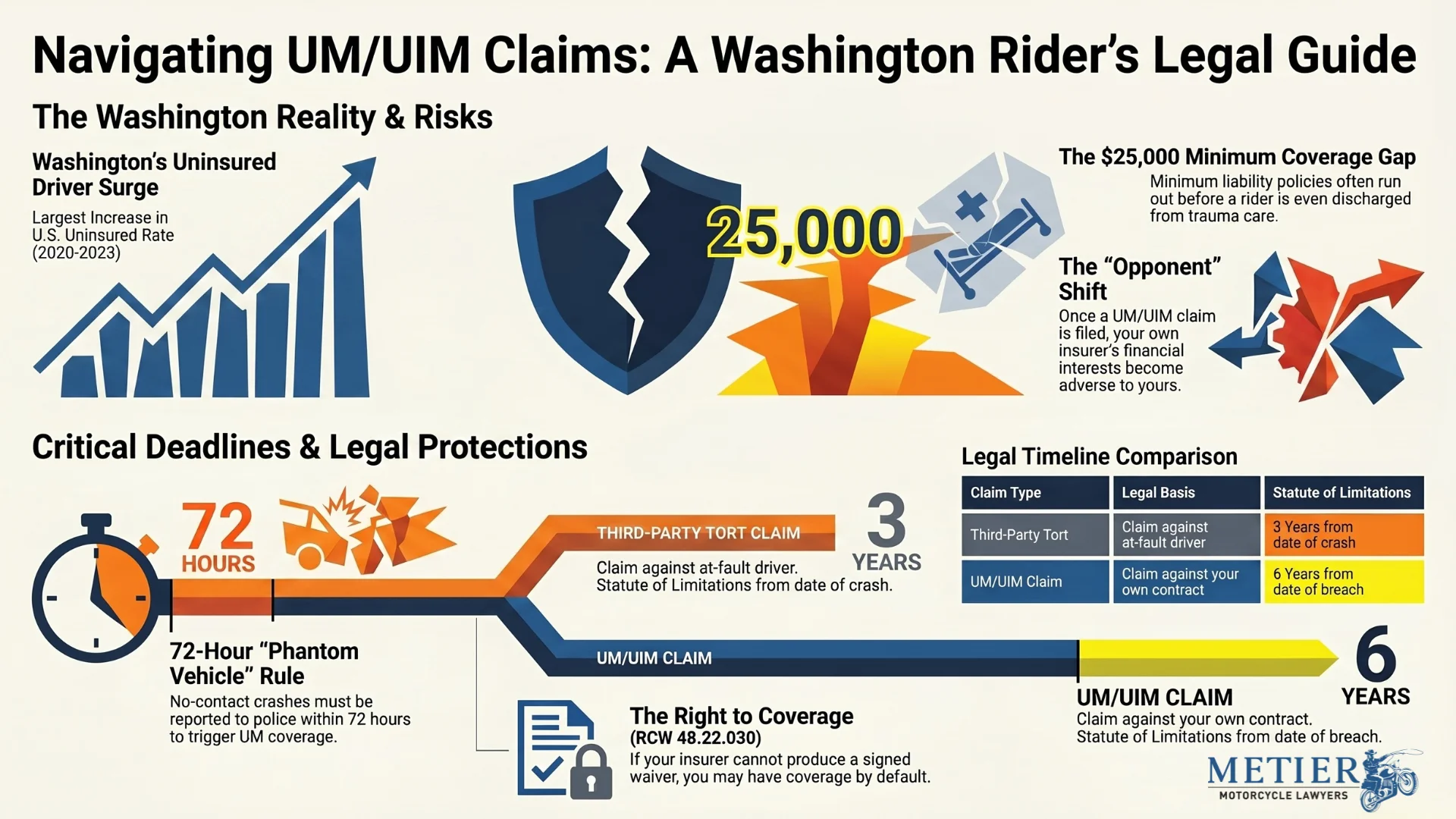

- If an uninsured or underinsured driver hits you on your motorcycle around Seattle or Tacoma, your own UM/UIM coverage is usually your main path to recovery, and Washington combines uninsured and underinsured protection under one statute, RCW 48.22.030.

- Washington saw the largest increase in its uninsured-driver rate of any state from 2020 to 2023, according to the Insurance Research Council, so the odds a rider gets hit by someone who cannot pay are climbing.

- A no-contact "phantom vehicle" crash can still trigger your UM coverage if you report it to police within 72 hours and back it up with evidence beyond your own word.

- Your insurer turns into your opponent the moment you file a UM/UIM claim, and the tactics they use to shrink rider payouts are predictable once you know them.

- Washington gives you more time than most riders think: a UM/UIM claim against your own insurer is a contract claim with a six-year deadline under Safeco Insurance Co. v. Barcom, not the three-year tort deadline, and that clock does not start until the insurer breaches the contract.

You are riding south on I-5 through the Seattle-Tacoma stretch, doing everything right, when a car drifts across a lane and puts you on the pavement. You find out at the hospital that the driver carried no insurance, or carried the bare state minimum that runs out before your first surgery is paid for. That second gut punch is the one we see flatten Washington riders financially, and it is the one most people never see coming.

"The crash is only the first problem," says Patrick DiBenedetto, Partner and Motorcycle Lawyer at Metier Law Firm, who rides himself. "The second problem is when you learn the driver who hit you has nothing to pay with. That is the moment your own uninsured motorist coverage either saves you or, if you waived it, leaves you holding a six-figure medical bill for a crash you did not cause."

This blog is about that second problem. Not what coverage you should buy, we cover that in our guide on whether motorcycle insurance is required in Washington State. This is about what an injured Seattle motorcycle uninsured motorist claim actually involves once the crash has already happened and the at-fault driver cannot make you whole.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

What UM and UIM Cover When You Are the One Hit

Uninsured motorist coverage (UM) pays your damages when the driver who hit you had no liability insurance at all, or fled and was never identified. Underinsured motorist coverage (UIM) pays the difference when the at-fault driver had some insurance, but not enough to cover what your injuries actually cost. Washington folds both into a single protection under RCW 48.22.030, and the statute's stated purpose is to protect innocent victims of underinsured drivers.

Here is why this matters so much for riders specifically. Washington's minimum liability requirement is $25,000 per person for bodily injury. A single night in a Seattle trauma center, plus surgery and follow-up, can pass that number before you are discharged. When the at-fault driver carries only the minimum, that $25,000 is gone fast, and your UIM coverage on your own policy becomes the only realistic source for the rest. A serious motorcycle crash routinely produces medical bills, lost income, and long recovery time that dwarf a minimum-limits policy.

For the exact coverage minimums and what Washington requires you to carry, our Washington motorcycle insurance requirements guide walks through the numbers. The point here is narrower: when the other driver's policy cannot cover your injuries, your UM/UIM claim is what stands between you and paying out of pocket.

Why Your Own Insurer Becomes the Opponent

A UM/UIM claim is different from a normal injury claim in one uncomfortable way. You are not filing against the other driver's company. You are filing against your own insurer, the company you have paid premiums to for years.

That changes the relationship. Your insurer's financial interest is now the opposite of yours. Every dollar they pay you on a UM/UIM claim is a dollar out of their pocket, and the adjuster handling your file knows it. They may still sound friendly. They will still call quickly. But the goal of that early call is to gather information they can use to value your claim as low as possible. Riders are especially exposed here, because adjusters lean on tired assumptions about motorcyclists being reckless to push fault and shrink payouts.

This is not a reason to panic. It is a reason to be careful about what you say and sign before you understand what your claim is worth.

The Washington Rules That Work in Your Favor

Washington law gives riders more protection than most people realize, and knowing these rules before you talk to your insurer matters.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

Your Insurer Had to Offer You This Coverage

Under RCW 48.22.030, insurers writing motorcycle policies in Washington must inform riders about UM/UIM coverage and give a written opportunity to reject it. If you never signed a valid written waiver, you may have coverage you did not know you had. Washington courts have held that if the insurer cannot produce a proper signed rejection, the coverage is treated as if it were in place at limits matching your liability coverage.

A Hit-and-Run Counts

If the driver who put you down fled and was never identified, Washington treats that as an uninsured motorist situation, and your UM coverage can apply.

A No-Contact Crash Counts as Well

Washington recognizes "phantom vehicle" claims, where a driver runs you off the road or forces you to crash without ever touching your bike. To use UM coverage in that situation, you must report the crash to law enforcement within 72 hours, and the facts have to be corroborated by evidence other than just your own testimony. The Washington State Office of the Insurance Commissioner confirms this same 72-hour phantom-vehicle reporting rule. That is why scene evidence, witness names, and a prompt police report matter so much for riders.

One more rider-specific point: since July 28, 2019, Washington has required all motorcyclists to carry liability coverage, ending the old exemption, per the Washington Office of the Insurance Commissioner. That history shapes how UM/UIM gets applied to riders today.

Insurer Tactics That Shrink Rider Payouts, and How to Counter Them

Once you file, the patterns are predictable. Three show up in almost every rider's UM/UIM claim:

The Early Recorded Statement

The adjuster asks if you can give a quick statement "just to get the details down." You do not have to, and in most cases you should not, at least not before talking with a lawyer. Those statements get mined for any phrase that lets them assign you fault or downplay your injuries.

The Fast, Low Offer

It arrives while you are still hurting and short on income, so it can feel like relief. It is almost always far below what a serious motorcycle injury is worth, and accepting it usually closes the claim for good.

The Fault Argument

Because Washington uses comparative fault, the adjuster has a direct financial reason to push your fault percentage up, since it reduces what they owe. They will scrutinize lane position, speed, and gear. If you were lane filtering when the crash happened, that gets used too, and our breakdown of Washington's lane filtering law and fault covers how that fight actually plays out. Wet-weather crashes get the same treatment, which we address in our post on wet-road motorcycle accidents on I-5.

The counter to all three is the same: preserve evidence early, say little to the adjuster, and get your claim valued by someone who handles motorcycle cases before you agree to anything.

If you've been hurt in a motorcycle crash and need answers, call us at 833-4MOTO-LAW (833-466-8652) or schedule a free consultation at www.metierlaw.com.

The Deadline That Surprises Riders, in a Good Way

Most people assume the three-year personal injury deadline that applies to suing the at-fault driver also applies to a claim against their own insurer. In Washington, it usually does not. Because a UM/UIM claim is a claim under your insurance contract, the Washington Supreme Court held in Safeco Insurance Co. v. Barcom that the six-year written-contract statute of limitations applies to a UM/UIM claim against your own insurer, not the three-year tort deadline. And that six-year clock does not start at the crash. It starts when the insurer breaches the contract, such as when it wrongfully refuses to pay what you are owed.

Washington courts have also held that an insurer generally cannot shorten that window through fine print unless the policy expressly and clearly displaces the statutory period. That is real protection for riders, and it is the opposite of what insurers often imply when they pressure you to settle fast.

None of this is a reason to wait. The separate claim against the at-fault driver still runs on Washington's three-year tort deadline, and evidence has its own clock no statute protects. Traffic camera footage along the I-5 corridor gets overwritten, witnesses move, and physical evidence on your bike and gear gets cleaned or repaired. The stronger move is to document the claim early and let the longer deadline be a safety net, not a strategy.

Frequently Asked Questions

Do I have to use my own insurance if an uninsured driver hits me on a motorcycle in Seattle?

If the at-fault driver had no insurance or fled, your own uninsured motorist coverage is usually your primary path to recovery in Washington. You file the claim with your own insurer under your UM coverage. This does not work like an at-fault claim where your rates are punished for someone else's negligence, it is the coverage you paid for precisely so it would be there in this situation.

What if the driver who hit me had insurance but not enough?

That is what underinsured motorist coverage is for. When the at-fault driver's policy limit is lower than your actual damages, your UIM coverage can pay the difference up to your own policy limit. With Washington's minimum liability at $25,000 per person, a serious motorcycle injury often exceeds the at-fault driver's coverage quickly, which is exactly when UIM matters most.

I never bought UM/UIM coverage for my motorcycle. Am I out of luck?

Not necessarily. Under RCW 48.22.030, your insurer was required to offer the coverage and obtain a written rejection if you declined it. If they cannot produce a valid signed waiver, Washington law may treat your policy as carrying UM/UIM coverage at limits matching your liability coverage. It is worth having an attorney review your policy and the insurer's records before you assume you have no coverage.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

A car ran me off the road but never touched my motorcycle. Can I still file a UM claim?

Possibly. Washington recognizes phantom vehicle claims for no-contact crashes. To qualify, you must report the crash to law enforcement within 72 hours, and the facts must be supported by evidence beyond your own testimony, such as witness statements or physical evidence. This is one of the strongest reasons to call police and gather witness information at the scene, even when the other vehicle is already gone.

How long do I have to file a UM/UIM claim in Washington?

A UM/UIM claim against your own insurer is treated as a contract claim in Washington, so the six-year written-contract statute of limitations applies rather than the three-year tort deadline, under Safeco Insurance Co. v. Barcom. That clock does not start at the crash, it starts when the insurer breaches the contract, such as by wrongfully refusing to pay. That said, the separate claim against the at-fault driver still runs on the three-year tort deadline, and evidence fades fast, so it is still smart to document the claim and have your policy reviewed early rather than relying on the longer window.

Motorcycle Riders Should Not Have to Fund Someone Else's Mistake

When an uninsured or underinsured driver puts you down on I-5 or anywhere around Seattle or Tacoma, the law does not leave you with nothing, but the path to recovery runs through your own insurer, and that company is not on your side once the claim is filed. We are riders who handle these claims, we know how Washington's UM/UIM rules work, and we know the tactics insurers use to pay riders less than they are owed. Serving riders across Seattle, Tacoma, and Washington, we fight to make sure the coverage you paid for actually shows up when you need it.

Our motorcycle accident attorneys have handled UM/UIM claims like these for years, and as a Seattle motorcycle accident lawyer team, we know exactly how local insurers try to shrink these payouts. When a crash like this proves fatal, a Seattle wrongful death lawyer from our team stands with the family through everything that follows.

Call Metier Motorcycle Lawyers at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today.

Disclaimer: Past results discussed should not be considered a guarantee of your results as the factors of every case are individually unique. This content is for informational purposes only and does not constitute legal advice. Consult a qualified attorney from Metier Law Firm regarding your individual situation for legal advice.

Related Blog Posts

When Your Passenger Is Hurt: Motorcycle Passenger Injury Claims in Fort Collins

When Your Passenger Is Hurt: Motorcycle Passenger Injury Claims in Fort Collins UM/UIM Coverage for Cheyenne Motorcycle Riders: What Riders Need to Know Before a Crash

UM/UIM Coverage for Cheyenne Motorcycle Riders: What Riders Need to Know Before a Crash Rear-Ended on a Motorcycle in Colorado Springs: Who's at Fault and What to Do

Rear-Ended on a Motorcycle in Colorado Springs: Who's at Fault and What to DoIf You've Been Injured In A Motorcycle Crash, Call Today - (833) 4MOTO-LAW

Tell Us About Your Case – Free Case Review with a Personal Injury Lawyer

(866) 377-3800Our Locations

.webp)

Do I have a Case?

How Much Should I Be Offered?

Do I Need an Attorney?

If these questions have crossed your mind, let us help. You may need a little direction or may not need an attorney at all, but you deserve to be confident knowing your options. We can provide you with information about our Attorneys of the West® accident investigations and legal services. Your confidential consultation with us is totally free.

Keep up with us!