.svg)

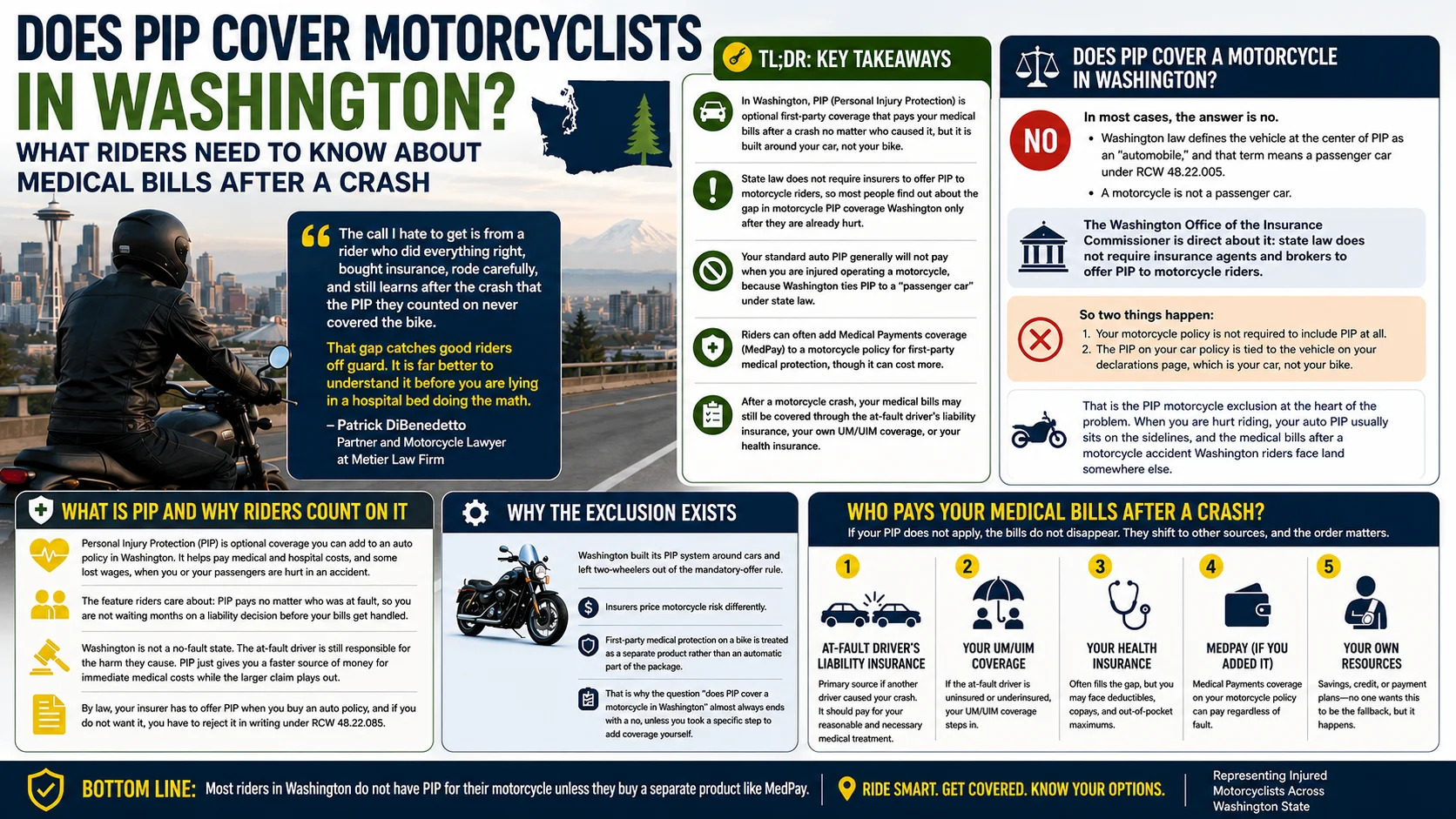

TL;DR: Key Takeaways

- In Washington, PIP (Personal Injury Protection) is optional first-party coverage that pays your medical bills after a crash no matter who caused it, but it is built around your car, not your bike.

- State law does not require insurers to offer PIP to motorcycle riders, so most people find out about the gap in motorcycle PIP coverage Washington only after they are already hurt.

- Your standard auto PIP generally will not pay when you are injured operating a motorcycle, because Washington ties PIP to a "passenger car" under state law.

- Riders can often add Medical Payments coverage (MedPay) to a motorcycle policy for first-party medical protection, though it can cost more.

- After a motorcycle crash, your medical bills may still be covered through the at-fault driver's liability insurance, your own UM/UIM coverage, or your health insurance.

You go down at an intersection in Seattle. Maybe a driver turned left across your lane on Rainier Avenue, or someone merged without looking on the way through Federal Way. The ambulance ride and the emergency room visit start adding up before you have even left the building. You assume the PIP on your insurance will handle that first wave of medical bills, the way it would after a car accident. Then you learn it does not apply to your motorcycle at all.

That is one of the most common and painful surprises we see from riders across Washington, from Seattle and Bellevue down to Tacoma. Understanding how motorcycle PIP coverage Washington works, and where it stops, can save you from a financial blow at the worst possible time. Patrick DiBenedetto, Partner and Motorcycle Lawyer at Metier Law Firm, has represented injured riders for years, and he rides himself.

"The call I hate to get is from a rider who did everything right, bought insurance, rode carefully, and still learns after the crash that the PIP they counted on never covered the bike," says Patrick DiBenedetto. "That gap catches good riders off guard. It is far better to understand it before you are lying in a hospital bed doing the math."

What PIP Is and Why Washington Riders Count On It

Personal Injury Protection is optional coverage you can add to an auto policy in Washington. It helps pay medical and hospital costs, and some lost wages, when you or your passengers are hurt in an accident. The feature riders care about is that PIP pays no matter who was at fault, so you are not waiting months on a liability decision before your bills get handled.

Washington is not a no-fault state. The at-fault driver is still responsible for the harm they cause. PIP just gives you a faster source of money for immediate medical costs while the larger claim plays out. By law, your insurer has to offer PIP when you buy an auto policy, and if you do not want it, you have to reject it in writing under RCW 48.22.085. A lot of drivers have it and do not even remember saying yes. That is the promise behind motorcycle PIP coverage Washington riders hope to lean on, and it is exactly where the trouble starts.

Does PIP Cover a Motorcycle in Washington?

When it comes to motorcycle PIP coverage Washington law draws a clear line, and it is not the one riders expect. In most cases, the answer is no. Washington law defines the vehicle at the center of PIP as an "automobile," and that term means a passenger car under RCW 48.22.005. A motorcycle is not a passenger car. On top of that, the Washington Office of the Insurance Commissioner is direct about it: state law does not require insurance agents and brokers to offer PIP to motorcycle riders.

So two things happen. Your motorcycle policy is not required to include PIP at all, and the PIP on your car policy is tied to the vehicle on your declarations page, which is your car and not your bike. That is the PIP motorcycle exclusion at the heart of the problem. When you are hurt riding, your auto PIP usually sits on the sidelines, and the medical bills after a motorcycle accident Washington riders face land somewhere else.

Why the Exclusion Exists

None of this is an oversight. Washington built its PIP system around cars and left two-wheelers out of the mandatory-offer rule. Insurers price motorcycle risk differently, and first-party medical protection on a bike is treated as a separate product rather than an automatic part of the package. That is why the question "does PIP cover a motorcycle in Washington" almost always ends with a no, unless you took a specific step to add coverage yourself.

What This Means for Your Medical Bills After a Crash

Once you understand the limits of motorcycle PIP coverage Washington offers, the next question is who actually pays. If your PIP does not apply, the bills do not disappear. They shift to other sources, and the order matters.

The at-fault driver's liability insurance is the primary target. If another driver caused your crash, their bodily injury coverage should pay for your injuries. The catch is that Washington only requires $25,000 per person in liability coverage, and a serious motorcycle injury can exceed that limit quickly.

Your own uninsured and underinsured motorist coverage is the next layer. If the driver who hit you had no insurance or not enough, UM/UIM on your motorcycle policy can help fill the gap. Your rights as an injured Washington rider do not vanish just because your PIP never applied.

Health insurance can also cover treatment, though you may deal with deductibles, copays, and a reimbursement demand later.

MedPay on a Motorcycle Policy

The cleanest fix is to add first-party medical coverage to your motorcycle policy before a crash ever happens. While you can actually purchase a separate motorcycle PIP policy in Washington, it is notoriously hard to find and expensive. As a result, many riders choose Medical Payments coverage (MedPay) instead. Both options work like auto PIP by paying your medical bills regardless of fault, and while insuring a bike costs more than a car, that protection is well worth it if you are staring down a hospital bill.

If you've been hurt in a motorcycle crash and need answers, call us at 833-4MOTO-LAW (833-466-8652) or schedule a free consultation at www.metierlaw.com.

How to Protect Your Coverage Before You Ride

A few minutes with your policy now can save you a lot later. Pull your declarations page and see what is actually listed. Washington already requires liability insurance on your motorcycle, and we break those requirements down in our post on whether motorcycle insurance is required in Washington. Liability protects other people, though, not you.

Ask your agent three questions. Does my motorcycle policy include MedPay, and how much. Do I carry UM/UIM on the bike. And is there any first-party medical coverage that applies while I am riding. If you have already been in a crash, our guidance on what to do after a Seattle motorcycle crash walks through the steps that protect both your health and your claim.

Getting this right is the difference between a Washington motorcycle insurance after a crash headache and a plan you can actually rely on.

Frequently Asked Questions

Does PIP cover a motorcycle in Washington?

Usually no. Washington's PIP system is built around a passenger car, and state law does not require insurers to offer PIP to motorcycle riders. The PIP on your auto policy is tied to the car on your declarations page, so it generally will not pay when you are injured on your motorcycle.

Is PIP required in Washington?

No. PIP is optional even for car owners. Your insurer must offer it, but you can reject it in writing. For motorcycles, insurers are not even required to offer it in the first place. You can purchase a separate PIP policy for your motorcycle however it is expensive and difficult to find.

Who pays my medical bills after a motorcycle accident in Washington?

If another driver caused the crash, their liability insurance is the first source. After that, your own UM/UIM coverage, MedPay on your motorcycle policy, or your health insurance may apply. Sorting out that order is a big part of any Washington motorcycle accident insurance claim.

Can I add first-party medical coverage to my motorcycle policy?

Yes. Many riders add MedPay to their motorcycle policy, which pays medical bills regardless of fault. It is the most direct way to get the first-party medical coverage motorcycle WA policies can provide, though it typically costs more than PIP does on a car.

What is the PIP exclusion for a motorcycle?

It refers to the reason your auto PIP does not follow you onto your bike. Because Washington ties PIP to a passenger car, your motorcycle sits outside that coverage, which is why so many riders discover the gap only after a crash.

Riders Shouldn't Have to Learn This the Hard Way

The hardest conversations we have start with a rider who assumed their motorcycle PIP coverage Washington would be there and found out too late that it was not. You can get ahead of that. Check your policy, ask about MedPay and UM/UIM, and know where your medical bills would land before you ever need the answer. And if a crash has already happened, you do not have to work out the coverage puzzle alone. Our team of Seattle motorcycle accident lawyers rides these same roads and knows exactly how Washington insurers handle these claims. Call Metier Motorcycle Lawyers at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com.

Disclaimer: Past results discussed should not be considered a guarantee of your results as the factors of every case are individually unique. This content is for informational purposes only and does not constitute legal advice. Consult a qualified attorney from Metier Law Firm regarding your individual situation for legal advice.

Related Blog Posts

Rear-Ended on a Motorcycle in Colorado Springs: Who's at Fault and What to Do

Rear-Ended on a Motorcycle in Colorado Springs: Who's at Fault and What to Do Lane-Change and Blind-Spot Motorcycle Crashes in Denver: When a Car Merges Into a Motorcycle Rider

Lane-Change and Blind-Spot Motorcycle Crashes in Denver: When a Car Merges Into a Motorcycle Rider Oregon Motorcycle Camping Guide: Best Day and Weekend Rides From Portland for Summer Riders

Oregon Motorcycle Camping Guide: Best Day and Weekend Rides From Portland for Summer RidersTell Us About Your Case – Free Case Review with a Personal Injury Lawyer

(866) 377-3800Our Locations

.webp)

Do I have a Case?

How Much Should I Be Offered?

Do I Need an Attorney?

If these questions have crossed your mind, let us help. You may need a little direction or may not need an attorney at all, but you deserve to be confident knowing your options. We can provide you with information about our Attorneys of the West® accident investigations and legal services. Your confidential consultation with us is totally free.

Keep up with us!