.svg)

TL;DR: Key Points

- Wyoming requires insurers to offer UM/UIM coverage, but you can waive it in writing — and many riders do without understanding what they're giving up.

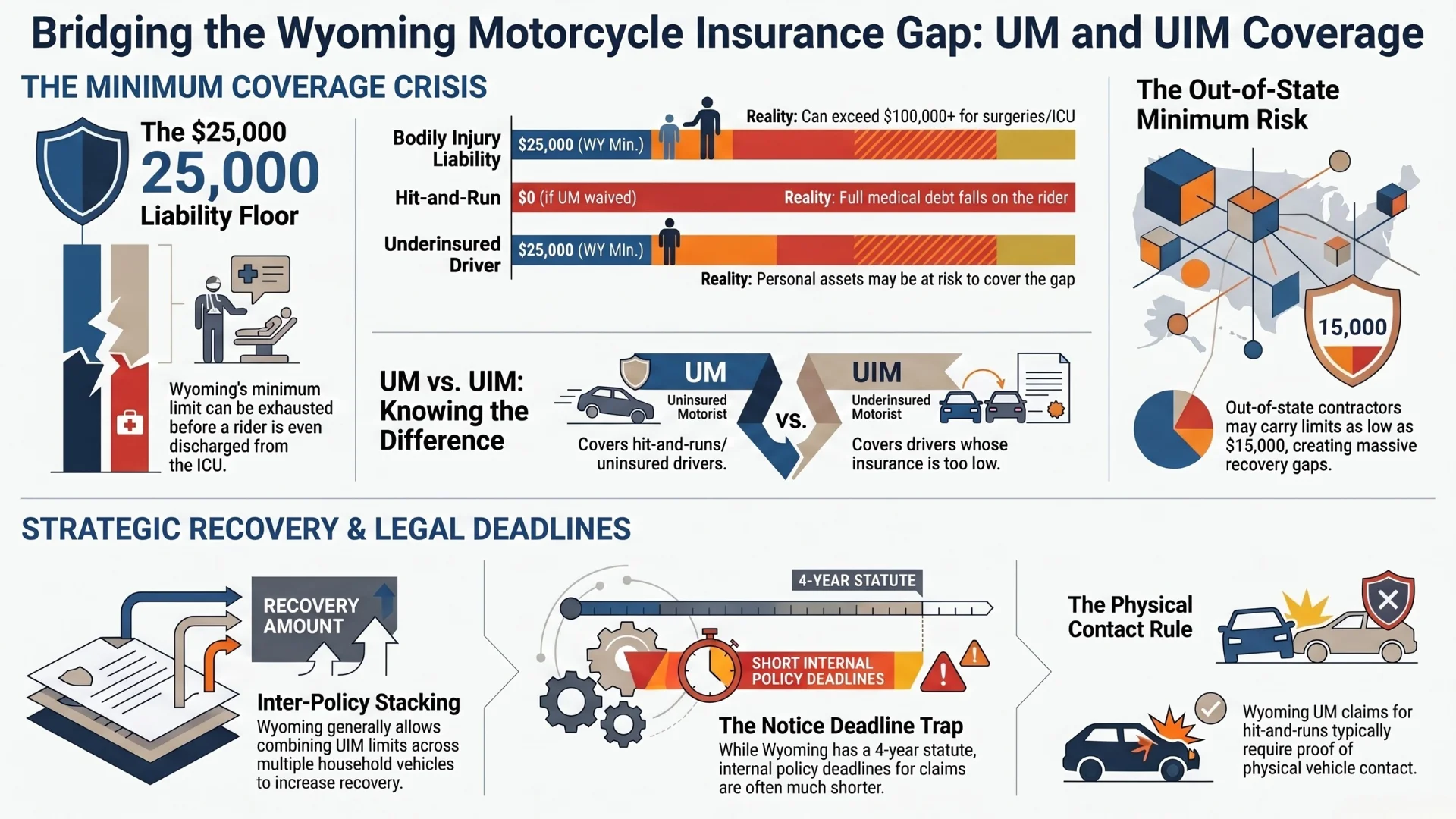

- Wyoming's minimum liability limit is $25,000 per person. One night in the ICU can exceed that. When the at-fault driver's policy runs dry, UIM on your own policy is often the only realistic recovery source.

- A hit-and-run on I-25, US-20/26, or WY-220 is treated as an uninsured motorist event under Wyoming law — your UM coverage applies if you have it.

- Wyoming generally permits stacking of UIM coverage across separate policies, unless your insurer has a clear anti-stacking provision in writing. If you've got multiple bikes or vehicles in your household, it's worth checking.

- Wyoming's statute of limitations for personal injury is four years (W.S. § 1-3-105), but UM and UIM claims have their own notice deadlines buried in your policy. Waiting costs you.

You're riding west on US-20/26 outside of Mills, headed toward Riverton. A pickup pulls out from a side road and clips your front wheel. You go down hard. The other driver has insurance — technically. His policy carries $25,000 in bodily injury coverage. Your collarbone is shattered, your knee needs surgery, and you haven't gotten to the ambulance bill yet.

That $25,000 is gone before you're discharged.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

This is where most Casper riders find out they have a gap. Not because the other driver was uninsured. Because he was underinsured — carrying Wyoming's minimum liability limits on a crash that costs three or four times that amount. If you don't have underinsured motorist coverage on your own policy, you're left trying to collect from someone who doesn't have more to give.

"This is the scenario I see most often from riders in central Wyoming," says Patrick DiBenedetto, Partner at Metier Law Firm and a rider himself. "It's not the uninsured driver people think they need to worry about. It's the driver who technically has insurance, but whose policy maxes out on the first day of your hospital stay. Without UIM coverage, we're starting from a very difficult position."

Understanding how uninsured motorist coverage Wyoming motorcycle policies provide — and how UIM fills the gap when minimum limits run short — is one of the more important things a Casper-area rider can do before a crash happens.

What UM and UIM Actually Cover

These two coverages get lumped together, but they work differently.

Uninsured Motorist (UM) Coverage

UM pays for your injuries when the at-fault driver has no liability insurance at all. In Wyoming, insurers are required to offer it, but you can reject it in writing. A lot of riders do, often without fully understanding what they're giving up.

UM also applies to hit-and-run crashes. If you're hit on I-25 through downtown Casper and the driver takes off, that's a UM event. Wyoming does require that the facts of a hit-and-run be provable — physical contact must have occurred, and the insurer can require corroborating evidence beyond your own testimony. Getting law enforcement to the scene immediately and locking down witness information matters here more than in almost any other scenario.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

Underinsured Motorist (UIM) Coverage

UIM covers the gap when the at-fault driver has insurance, but not enough. Wyoming minimum liability is $25,000 per person. For a crash that results in a femur fracture, a traumatic brain injury, or spinal damage, that number doesn't approach actual losses. Your UIM policy covers the difference between what the at-fault driver's policy pays and your total damages — up to your own UIM limit.

Wyoming also has no personal injury protection (PIP) requirement. There's no no-fault system here. If the at-fault driver is underinsured and you haven't purchased UIM, your options narrow fast to suing a defendant who may have nothing worth collecting.

Why the Casper Market Creates Specific Risk

Wyoming's overall uninsured driver rate is relatively low compared to the national average. According to the Insurance Research Council's most recent study, cited by the NAIC, 15.4% of U.S. motorists were uninsured in 2023 — roughly one in seven drivers. Wyoming sits well below that figure. But the question for a rider on WY-220 heading toward Alcova, or on US-20/26 through the energy traffic west of Casper, isn't just whether the driver behind them has insurance. It's whether that policy is enough to cover a real crash.

The energy workforce moving through Natrona County creates a specific version of the underinsured problem. Out-of-state contractors rotate in and out on job cycles, some driving personal vehicles registered elsewhere with other states' minimum coverage. Those minimums vary. A driver from a state with a $15,000 per-person floor is carrying even less than Wyoming's minimum. When that driver is at fault on Hat Six Road or north toward Midwest, the recovery ceiling is low — and there's no PIP system to bridge the gap.

Three Casper-area scenarios we see regularly:

Hit-and-run on I-25 through downtown Casper

Traffic picks up on the interstate corridor through the city. A driver clips you and keeps going. Without UM coverage on your own policy, there's no realistic path to recovery for your injuries. With it, you have a claim — but the physical-contact and corroboration requirements mean evidence gathered at the scene is everything.

Out-of-state minimum-limit driver on US-20/26

The corridor west toward Mills and Riverton runs through active energy traffic. A contractor driving a personal truck with bare-minimum out-of-state coverage is a UIM problem the moment your medical bills exceed their policy limit. That happens fast.

Low-coverage driver on WY-220

Summer recreational traffic to Pathfinder and Alcova brings drivers from across Wyoming and beyond. Some carry minimum coverage or carry coverage they haven't updated in years. When a crash happens on that road, UIM is often the only coverage that actually pays.

If you've been hurt in a motorcycle crash and need answers, call us at 833-4MOTO-LAW (833-466-8652) or schedule a free consultation at www.metierlaw.com.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

Stacking UIM Coverage in Wyoming

Stacking means combining UIM limits across multiple policies or vehicles. If you and your household have two bikes and a car, each carrying a separate policy with UIM limits, stacking lets you pool those limits for a single claim.

Wyoming generally allows inter-policy stacking — combining UIM limits across separate policies — unless your insurer has included clear and unambiguous anti-stacking language. The Wyoming Supreme Court established in Aaron v. State Farm Mut. Auto. Ins. Co., 34 P.3d 929 (Wyo. 2001), that no public policy bars stacking when an insured has paid separate premiums on separate policies. The 10th Circuit applied Wyoming law to this question in Mena v. Safeco Ins. Co., 412 F.3d 1159 (10th Cir. 2005), ultimately upholding an anti-stacking clause because the policy language was clear and unambiguous — which also illustrates exactly what to look for in your own policy. If the language isn't explicit, stacking is generally permitted under Wyoming law. Intra-policy stacking — combining limits within a single multi-vehicle policy — depends on how that specific policy is written.

If your household runs more than one vehicle, the practical question is whether each policy was purchased separately with separate premiums paid. If so, you may have more UIM coverage available than you realize.

Pull your policies out and read the UIM sections. If the stacking language isn't clear, that's worth a call to a Casper motorcycle accident lawyer — not your insurer.

Helmet Use, Comparative Fault, and Your UIM Claim

Wyoming's modified comparative fault rule (W.S. § 1-1-109) bars recovery if you're found 51% or more at fault. At 50% or less, your damages are reduced proportionally. This applies to UM and UIM claims too.

What some riders don't realize is that riding without a helmet — which is legal for adults in Wyoming under WYDOT guidelines — can become a fault argument on the injury side of your claim. The at-fault driver's insurer, or your own insurer on a UIM claim, may argue that your head or neck injuries were made worse by riding without head protection. They can't attribute the crash to you on that basis. But they can try to inflate your comparative fault percentage on injury-specific damages and reduce what you recover.

We've seen this in Casper-area claims. It's counterable — but it's easier to counter when a lawyer gets involved early. For a full breakdown of how fault arguments play out in central Wyoming motorcycle cases, see our guide on how fault works in a Casper motorcycle accident.

The Statute of Limitations Is Four Years — but Your Policy May Not Wait

Wyoming gives you four years from the date of a motorcycle crash to file a personal injury lawsuit against the negligent party under W.S. § 1-3-105. That sounds like room to breathe. It isn't, in practice.

UM and UIM claims are different from third-party liability claims. Your own insurance policy will have notice requirements and deadlines for asserting a UIM claim that are separate from the state statute. Some policies require notice within 30 days of identifying an underinsured motorist situation. Miss that window and you may forfeit the right to claim, regardless of where you stand on the four-year state deadline.

The sooner a motorcycle accident attorney in Casper reviews your policy, the better. Physical evidence disappears. Witnesses move. And your policy's internal clocks start running whether you're aware of them or not. For more on why the road hazards in this area generate crashes in the first place, see our post on motorcycle accident risks in Casper.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

Frequently Asked Questions: Wyoming Motorcycle UM and UIM Coverage

Does my motorcycle insurance in Wyoming automatically include UM/UIM coverage?

No. Wyoming law requires insurers to offer UM/UIM coverage, but you can reject it in writing. If you signed a rejection form when you bought your policy, you likely don't have it. Check your declarations page. If you see a UM/UIM line with limits listed, you have it. If not, call your insurer and ask directly — don't assume.

If I'm hit by an uninsured driver on a Wyoming highway, what actually happens?

If you have UM coverage, your own policy steps in to cover your injuries up to your coverage limits. Wyoming requires physical contact for a hit-and-run UM claim, and corroborating evidence beyond your own statement is typically required. A police report from the scene is your most important asset. Our Casper motorcycle accident lawyer team handles these claims regularly.

What is the difference between uninsured and underinsured motorist coverage in Wyoming?

UM covers you when the at-fault driver has no liability insurance at all. UIM coverage applies when the at-fault driver has insurance, but not enough to cover your actual damages. Wyoming's minimum is $25,000 per person — for serious motorcycle injuries, that's often exhausted in the first week of treatment. UIM fills the gap between their limit and your real losses.

Can I stack UIM coverage across my bikes and household vehicles in Wyoming?

Generally yes, if you paid separate premiums on separate policies and those policies don't contain clear anti-stacking language. Wyoming courts have upheld stacking under those circumstances. Intra-policy stacking depends on specific policy language. Check for anti-stacking provisions and talk to a Casper motorcycle accident lawyer if the language isn't clear.

How long do I have to file a UM/UIM claim in Wyoming?

The state's personal injury statute of limitations is four years under W.S. § 1-3-105, but your policy will have its own shorter internal deadlines for notifying your insurer and asserting a UIM claim. Missing those policy deadlines can result in a denial even if you're within the state's legal window. Contact a motorcycle accident attorney in Casper as soon as possible after your crash.

Call Metier Law Firm at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com

When the At-Fault Driver's Policy Isn't Enough

The roads around Casper are genuinely good riding country. But I-25, US-20/26, and WY-220 are also working roads — energy traffic, out-of-state drivers, wildlife crossings, wind that doesn't care about your lane position. When a crash happens out here, the at-fault driver's coverage often doesn't match what a serious motorcycle injury actually costs.

At Metier Motorcycle Lawyers, we've helped Wyoming riders pursue UM and UIM claims when the other driver's policy ran out, when hit-and-run drivers disappeared, and when insurers tried to use comparative fault arguments to shrink what a rider could recover. We know Wyoming law. We know this terrain. And we know what it takes to get a fair result when the coverage math doesn't work in your favor.

The Wyoming motorcycle insurance gap isn't always about uninsured drivers. Most of the time it's about minimum-limit policies and a state with no PIP cushion to soften the blow. Review your coverage now, before you need it.

Call Metier Motorcycle Lawyers at 833-4MOTO-LAW (833-466-8652) or schedule your free consultation today at www.metierlaw.com.

Disclaimer: Past results discussed should not be considered a guarantee of your results as the factors of every case are individually unique. This content is for informational purposes only and does not constitute legal advice. Consult a qualified attorney from Metier Law Firm regarding your individual situation for legal advice.

Related Blog Posts

Does Wyoming Require Motorcycle Helmets? What Cheyenne Riders Should Know Before and After a Crash

Does Wyoming Require Motorcycle Helmets? What Cheyenne Riders Should Know Before and After a Crash Top 10 Colorado Motorcycle Rides for Every Skill Level

Top 10 Colorado Motorcycle Rides for Every Skill Level Motorcycle Crashes in Larimer County: Rider Statistics and Seasonal Risk Trends for Fort Collins

Motorcycle Crashes in Larimer County: Rider Statistics and Seasonal Risk Trends for Fort CollinsTell Us About Your Case – Free Case Review with a Personal Injury Lawyer

(866) 377-3800Our Locations

.webp)

Do I have a Case?

How Much Should I Be Offered?

Do I Need an Attorney?

If these questions have crossed your mind, let us help. You may need a little direction or may not need an attorney at all, but you deserve to be confident knowing your options. We can provide you with information about our Attorneys of the West® accident investigations and legal services. Your confidential consultation with us is totally free.

Keep up with us!